Who Invented Blockchain?

Blockchain technology was first introduced in 1991 by Stuart Haber and W. Scott Stornetta, two mathematicians who wanted to apply a system where document time prints couldn’t be tampered with. In the late 1990s, cypherpunk Nick Szabo proposed using a blockchain to secure a digital payments system, known as a bit gold (which was noway administered). Finally, Blockchain was invented by Satoshi Nakamoto in 2008 and provided the first public ledger to user in basis of bitcoin cryptocurrency.

What Is a Blockchain?

We can predicate the meaning of Blockchain according to its name, buildings its data into chunks ( blocks) that are threaded together.

A blockchain is a distributed database that’s participated among the nodes of a computer network. As a database, a blockchain stores information electronically in digital format. Blockchains are best known for their key purpose in cryptocurrency systems, similar as Bitcoin, for maintaining a secure and decentralized record of transactions. This technology works to save the entire track record of deals of assets done in the business network. In simple language, all the deals on the blockchain network can be tracked practically and this also helps in preventing online frauds.

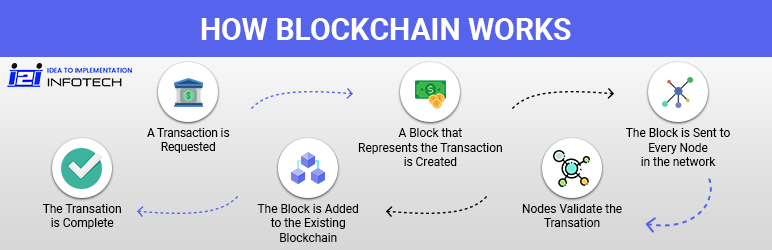

How Does a Blockchain Work?

A blockchain collects information together in groups, known as blocks, that hold sets of information. Blocks have certain storehouse capacities and, when filled, are closed and linked to the preliminarily filled block, forming a chain of data known as the blockchain.

The aim of blockchain is to allow digital information to be stored and distributed, but not edited. In this way, a blockchain is the foundation for unchangeable checks, or records of deals that can not be altered, deleted, or destroyed. That is the reason why blockchains are also known as a DLT(distributed ledger technology).

Blockchain Decentralization

Blockchain technology is secure as it’s decentralized and distributed. There’s no single point of failure, which makes it much harder to lose. Hacking into one part of the system can not affect other corridors. Still, in the case of a private blockchain, this advantage is incompletely lost as they have a single point of control and a limited number of nodes. So users are not able to modify anything to the tally. Organizations operate these kinds of blockchains for their internal use, as it allows the company to control its own processes.

Is blockchain technology safe?

Blockchain technology achieves decentralized security and trust in various ways. To begin with, new blocks are always stored linearly and chronologically. Each of the blocks holds a unique hash number and a link that connects it to the former block. Every block is an important part of the sequence, and it can not be changed. However, the hash sum would alter, and the block would no longer be valid, hash code changes as well If there’s any change.

Due to the size of multiple cryptocurrency networks and their growing speed, the cost to pull off such a feat assembly could be unstoppable. This would be not only extremely costly but also likely fruitless. Doing such a thing would not go unnoticed, as network members would see drastic changes to the blockchain.

Difference between Blockchain and Banks system

Blockchains have been heralded as being a disruptive force to the finance sector, especially with the functions of payments and banking. Still, banks and decentralized blockchains are highly different.

Cryptocurrencies are digital wealth that act like traditional moneybags and can serve as means of exchange. They’re generally bought through crypto exchange platforms and stored in safe crypto wallets. These digital currencies are decentralized, and they operate in a truly secure way with minimum human dealings. As a result, numerous now classify them as the future of the finance sector.

Nowadays, Banks are the financial systems of the world. They offer monetary support like loans, savings, and other deals. However, unlike cryptos, they have numerous lapses since they’re centralized and subject to impulses. They’re also fairly slower than cryptos, and some charge too high interests on loans and some deals.

How Are Blockchains Used?

Presently, there are additional than other cryptocurrency systems running on a blockchain. Arguably the most logical use for blockchain is as a means to expedite the transfer of finances from one party to another. As noted, with banks removed from the equation, and confirmation of deals ongoing 24 hours a day, seven days a week, utmost deals reprocessed over a blockchain can be settled within a matter of seconds.

Blockchain also comes in particularly handy when it comes to covering fund chains. By removing paper-based trails, businesses should be suitable to pinpoint inefficiencies within their fund chains speedily, as well as to detect details in real-time. Further, blockchain would allow businesses, and conceivably indeed consumers, to view how products performed from a quality-control perspective as they traveled from their place of origin to the retailer.

Advantages of blockchain technology

Decentralization

This is the main point of blockchain technology, and the strong point is that to authenticate deals or operations no other example is needed to act as a conciliator, reducing deal confirmation times.

Network distribution

This point provides, at the same time, several benefits since, by having this network distributed, in the first case, no one owns the network, allowing different addicts to always have multiple clones of the same information.

Also, this characteristic makes it resistant and flexible to any type of failure since the fact that a node fails doesn’t indicate generalized failures in the network.

Likewise, having a distributed network means that there are virtually no crimes because the information must be confirmed by numerous participators in this network. Incorrect or bad information within the blockchain becomes virtually insolvable.

Low costs for addicts

The decentralized nature of Blockchain allows for the confirmation of person-to-person deals rapidly and securely. Barring the need for a conciliator reduces costs for addicts.

Disadvantages of blockchain technology

High-performance costs

Just as this technology represents low costs for addicts, unfortunately, it also implies high-performance costs for companies, which detainment its mass acceptance and performance.

Inefficiency

It’s ineffective to have several network addicts validating the same operations since only one will take the price decided from this mining process. This process and for the same reason of numerous addicts doing the same thing, also implies a huge waste of energy, not certifiably environmentally friendly technology.

Private keys

Inordinate security can also be an Achilles heel, in the case of private keys, as has been proved on numerous occasions, having lost them it becomes nearly insolvable to recover these keys, causing a problem, substantially, for all those holders of cryptographic values.

Storage

As the number of addicts grows, the number of operations that will be integrated into the blocks to be stored will also grow, so the space needed will also have to increase inside the miner’s computers, ultimately exceeding the capacity of the hard disks.

Severance

The lack of need for interposers will bring that, as Blockchain technology is embraced and applied, all these intermediation sectors for the confirmation of payments and processes will inescapably be reduced to the point of fading and, with it, the jobs needed for it’ll vanish.

Conclusion

In conclusion, Blockchain technology creates an endless and unchangeable record of every transaction. This impenetrable digital tally makes fraud, hacking, data theft, and information loss unsolvable. While blockchain technology has reshaped and decentralized monetary institutions, its usage possibilities are far more robust. So blockchain technology will rule over the world in future decades.

Great article.